How My Investing Philosophy Evolved Over The Last Decade 📖 Part 1

How My Investing Philosophy Evolved Over The Last Decade 📖 Part 1

Debt-free with >550k AUD in stocks at age 33, from $0 at 26 (not 'rich' but 'free'); Going against what society tells you financially in Australia, & rough financial plans for the future 💰

Hit the like if you found interesting💝 Helps give me some feedback

First part of two articles; second one on; How I Invest

0 - TLDR

1 - Quick Rant on Australian Property 🏠

2 - Young & Naive, Where to Start Investing? 🤔

3 - My Issues With; ‘FIRE’🔥Financial Independence Retire Early

4 - Peter Thornhill 🥸

5 - Asymmetrical Investing 📈 Doing a 180 on My Investing Philosophy

6 - Exiting the Workforce, Travelling & Playing the Waiting Game ✈️

7 - Wrap Up & Future Financial Plans 🌎

Never had a loan or been in debt (besides student debt, paid off).

Never touched crypto - no crypto pumps.

Quit my job in mid 2023 at 33 and have since watched the portfolio grind higher by about 200k, all while slow travelling Europe & now Latin America.

I realise that financial ‘success’ is all subjective. There are 24 year old entrepreneurs out there who are multi-millionaires, & others in their 50s who are paycheck to paycheck.

TLDR (too long didn’t read)

The below points are essentially how I ended up where I am right now; sitting in South America after travelling for 10+ months, at 34 with a stock portfolio north of half a mil (volatile but growing) and no plans to return to the workforce..

Fully aware that this could all go tits-up at any moment 🫠

Property investment and Australia’s obsession with it never sat well with me, even before I had any money.

Discovered the Financial Independence Retire Early ‘FIRE’ movement in my mid-20s - latched onto it (too hard), and started pumping 70%+ of my salary into amassing Vanguard ETFs & Aussie LICs. Always had a very disciplined savings rate, while most people around me bought cars and toys.

2019 - Met

through my mate in the villa I used to share with them in Bali in my late 20s. Started to listen to Fergs investing ideas after initially hearing them from (through Fergs old free newsletter).Late 2019 - Started to get convinced to take more risk; and wanted to enter the uranium trade.

2019/2020 - Stubbornly and stupidly had the idea that I wanted to hit 110 - 120k in passive ETF’s in the portfolio, before diversifying into ‘riskier’ single company stocks - If I’d jumped into uranium in 2019/2020 when I was thinking about doing so, I would have well over 1 million $ of paper wealth now.

2020 - Started my first (small) positions in uranium during the COVID crash.

Slowly convinced myself of

s style of asymmetrical investing over 2020 as I learnt more about it, and began pivoting into uranium and offshore oil drillers.Saw a few of my mates make some huge returns off the initial moves in uranium in 2020, felt proper investing FOMO for the first time (IYKYK 😣). Finally questioned my philosophy on the whole FIRE movement.

Early 2021 - dumped everything into uranium and offshore oil, better late than never, but still missed the big asymmetrical moves off the bottom (a hard/good life lesson here).

Watched some of the positions in the portfolio go into the red ~10% for most of 2021, but had conviction in the thesis. Kept adding as much salary as I could afford.

2022 - finally saw the portfolio grind higher. Started to take some small positions in coal mining companies (more on the coal trade in the future), but still putting most of my salary into uranium and offshore oil.

2023 - had enough capital with no debt to comfortably quit my job and go travelling for the long term - It was difficult to pull the pin as my career/ladder climbing was going well with a big salary and cushy job. Portfolio total return was marching towards 200% (since 2021, not too bad).

2024 - Portfolio north of half a million AUD and continuing to grind higher through gut-wrenching volatility as the energy thesis gains steam.

Enough to give me the confidence to not have to work again in the medium term, come over to Latin America to ‘geo-arbitrage’ expenses, while slow travelling and making memories - which is what is currently most important to me ($3 grand a month AUD for everything and you can live like a king in most areas in LatAm, some places as low as $1750 ish AUD, future post on this - though my budget is somewhat higher).

Now playing the waiting game in 2024, with plans to (hopefully!) start scaling out in 2025 - and then use capital from uranium stocks (hopeful it should be $400k minimum after tax, potentially more 🤞) to invest in a cashflow producing, location independent, online business portfolio (again more on this in the future).

Also, plans to use some of the capital to start building out a portfolio of coal mining companies for the long term (10 to 15 years) for cashflow - another TraderFerg idea. I’ve also another chunk of the portfolio in offshore oil service companies, which will probably hold and add to over the next 3 to 5 years.

Days when you open your account and you are up 20% on the day (happens occasionally), which usually means you’re down 25% the next day.

They say that psychologically, we tend to be somewhat hardwired on a spectrum as ‘savers’ or ‘spenders’; and I have heard numerous financial podcasts over the years espouse dating advice on this topic, i.e, if you tend to be a saver, you are going to have a hard time dating an extreme spender.

I have always been conservative in my thinking (though this tends to be detrimental from an entrepreneurial perspective), and tended to save money, though had zero idea what I was doing when I first started my career at 24.

1 - A Quick Rant on Australian Property 🏠

The psyche of Australian society is obsessed with property ownership - will flesh this out further in another separate post.

I should state here that I am the odd one out - which is the entire point of starting to write stuff on Substack. I usually feel more comfortable going against the grain of most societal programming. I am not ‘anti-property’ investing (not completely), just find the myopic view of the topic in Australia to be frustrating.

Property as an asset in Australia is a religion, and essentially the only measure amongst the vast majority in the land down under of one’s financial success. You are genuinely compared to, and looked down upon if you are entering your late 20s and early 30s without having ‘a foot on the property market’.

My own mum is a great gauge of the ‘average Jo’ (her name is actually Jo) and has badgered me from a young age, well before I had any money, to get into property (love ya mum 😅). I never knew why at the time, but the whole idea never sat well with me (not into much ‘woo’ crap, but gut instinct is a thing).

I could never understand why you would take out this monumental amount of leverage, particularly when you are young and have a low salary, to essentially lock yourself into wage slavery for 20/30+ years, only to get a very shitty ROI on a rental yield (for residential property), & all the expenses of the property falling to you, taxes, stamp duty etc AND having to deal with tenants.

Eventually, you will use some of the hard-earned equity that didn’t get paid as interest to the bank, to borrow MORE money (standard operating procedure in Australia) to take out further leverage and buy additional properties 🤯. It feels like a psyop to me, to keep us all working in indentured servitude forever..!

In Australia, the stockmarket is considered far riskier than the property market, it does my head in. An amazing thing about a stock portfolio is the liquidity. At any moment I can withdraw any amount of cash from my portfolio that will appear in my bank account in 2 to 3 days.

I know many people in Australia who believe they are ‘wealthy’ due to the equity in their property(s), but have zero liquidity on the asset (no marginal liquidity). Technically yes, they are wealthy and good on ‘em if this makes them happy; however, in my opinion, this is not freedom and does not resonate with how I like to live in my mid 30s.

This is not a stocks vs property rant, but this liquidity (lack thereof) ties into my thinking about having more optionality in your life while still young (and still getting great/better returns than property).

“Australians have a genetic defect – this love affair with property” - Peter Thornhill.

I can understand and empathise completely that most people want some form some sort of a nest, particularly if starting a family, & that similarly, most people have no desire to travel or move far from their place of birth (nothing wrong with this!).

Personally, from a young age I always thought that there has to be another way!

I will definitely start buying property one day. Probably in my 40s once I have already made money/have cashflow from stocks and online businesses. With my current line of thinking (who knows what I’ll think in 7 years!), I would only consider buying a property with limited leverage and not in Australia. If I want to eventually break tax ties with Aus, don’t think I’ll be able to own property there.

Lastly, I will admit that I have been betting against the Aussie property market for over a decade, and that although everything I said above is true, property investors only continue to become richer - egg on my face! 🍳

This is a whole separate issue that boils down to absolutely insane & unsustainable levels of immigration (keeps inflating the bubble) & also cronyism in the fact that 90%+ of Australian politicians have large multi-million dollar property portfolios. Another rant for another time 🥲

2 - Young & Naive, Where to Start Investing? 🤔

Once I came back from travelling as a 24 year old with no career experience and in debt a few grand to my parents; I went into about an 90k AUD salary working 2 weeks on, 1 week off in an open pit gold mine as a Graduate Mine Geologist (low $ by the standards at the time).

Straight away I naturally wanted to start saving and investing, though had no idea how. I opened up a CommSec account (Avoid Commonwealth Bank and the ‘Big 4’ banks at ALL costs if you are Australian..) and pondered what to put the first buy order on, while feeling intimidated at the time by all the financial jargon of stop losses, buy-sell spreads and conditional orders.

The only person on the minesite where I worked at the time whom I respected (most of my superiors were nuffys 🐑), was the 2IC mining engineer. I probably had little more than 10k to my name when I heard him talking about investing in mining companies, and how he had put $250k (🤯) into a small Australian startup gold producer called Emerald Resources (a super interesting story as the first Western mining company to go into production in Cambodia). EMR was my first stock investment at about 5k AUD.

I ended up selling EMR about 2.5 years later for a measly $1,000 gain 🤣 - but this 'failure’ in single company stock investment (speculation/gambling) is what initially made me find the passive nature of ETF’s & LICs appealing.

3 - My Issues With; ‘FIRE’ 🔥 Financial Independence Retire Early

No doubt anyone who has read this far would have heard of this ‘movement’, so I won’t go too much into the nuts and bolts of it here (click the title link above). Though my way of thinking financially now does not align at all with ‘FIRE’, it was an important part of the evolution of my investing philosophy.

This turned into a bit of a rant too, so strap in….

The basic tenets of FIRE are essentially;

Extreme frugality in until you hit your ‘fire’ number (agree with some aspects of this).

Investing your high savings rate (also a great thing) into passive ETFs and (to a lesser extent) LICs (Licensed Investment Companies), typically through dollar cost averaging.

Once you hit your FIRE Number (typically takes decades) you use the 4% rule to live (again relatively frugally) off the dividends/capital gain from your portfolio.

After discovering ‘FIRE’, I spent the next few years pumping as much capital as I could afford from my salary into Vanguard ETF’s, and the classic old Australian LICs.

As mentioned above - I would easily be a millionaire today if I had pivoted away from FIRE investing (in ETFs and LICs) and 100% embraced asymmetrical investing in 2020 🥲

The three Aussie FIRE blogs I used to follow closely back in my mid-late 20s were:

Aussie FireBug - AussieFireBug’s monthly networth updates actually helped inspire me to write here on Substack, and are still a great read.

Captain FI - Aussie commercial airline pilot who interestingly did the same course in website SEO that I completed in 2023. An interesting blog.

Strong Money Australia - Absolutely nothing in common with Dave now, but he seems like a good bloke!

Would still recommend people (Aussies) to check out the above blogs as there is a wealth of information in them; although I disagree with most of what they espouse now.

Blindingly Obvious Problems with FIRE (from my perspective) 🤔

The point above; investing your high savings rate into passive ETFs and LICs, through dollar cost averaging, I believe is great for 80% of people who want to start investing for their future, and/or as an alternative to property investing. It certainly makes sense on paper and resonated me at the time as a 26 year old.

The main issues are:

Most of the FIRE ideology doesn’t align with my views on how you should experience the world in your 20s/30s, as it typically discourages spending money on longer term travel & life experiences.

I do not advocate for full YOLO dumbass spending on such things - I used to meet many cashed-up young lads in mining, who would ‘boast’ about how they spent 80 grand on their 6 month EuroTrip or 10 months in South America 🤦♂️; BUT I strongly believe that we can only have certain experiences at certain stages of our life.

The idea of saving for 20 years to finally go travel in your 40s or 50s carries a huge opportunity cost, not only could you die before you get there, but the experiences you have in your 20s you can never really have again (and everyone should experience them). No one wants to be the 39 year old bloke at a hostel bar, we’ve all seen them.

Even now at 34, I still absolutely still love travelling (hope to spend the rest of my 30s living overseas), but I barely drink/go out anymore, tend to base up in one spot for weeks at a time, and prefer hiking & chillin in cafes. I am super thankful of (most of) the degenerate/dumb experiences in my 20s.

I agree 💯 that people should aim to increase their savings rate to >50% while they’re young, without debt or dependants. However, skimping on coffees is not what moves the needle!

What moves the needle is increasing your salary/income as quickly as possible (if you save it!).

Do not emotionalise you career, it doesn’t care about you (it’s hard sometimes when you spend years studying)! Take pride in your work obviously, but you should prioritise the best ROI on your salary as a function of time, certainly prioritise this over climbing the corporate ladder (only aim to climb the ladder if the increase in income vs responsibility is worth it).

Remember, I am speaking to people here who want to ‘retire early’, not who want to retire at 60+ with a gold watch ⌚.

An example for me personally; if things go tits-up in the next 6 - 18 months (portfolio tanks due to another Fukishima), I would aim to find the highest paying geology contract gig with the lowest responsibility, and be very unlikely to take another senior position (high responsibility), stack shekels again for 6 to 12 months and then GTFO, using the capital to start my own online business (freedom).

My strongest disagreement with the FIRE ideology is The 4% Rule (call it 3% rule if you want). According to FIRE philosophy, we stack shekels and avoid treating ourselves during the prime of our lives, to finally take out 4% off our portfolio in ‘retirement’. Fair enough!

So, 4% of $1,000,000 is $40k; or I’ll be generous, 4% of $1.5 mil is $60 (annually).

I don’t know about you, but the idea of sacrificing my 20s, 30s & potentially 40s to live off 60 grand is an insanely bad deal. $60k annually in your 40s! Fk that!

Life Goals: I’d like to have at least 2 kids in my 40s, maybe more(depending on wealth..); I want to (eventually) start buying property in different countries, & I want to fund my life with cashflow of (hopefully at least) $20 grand USD per month. This is a separate post, but these are my current lofty goals. $60 grand a year? Nahhh.

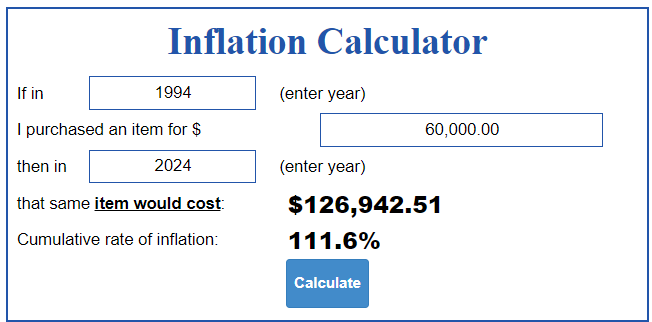

Ok, but the MAIN problema with the 4% rule is inflation - Inflation is running WAY hotter than any governments would have you believe (check out ShadowStats to see how much the government are cooking the books on this, they don’t even measure inflation the same way as they did in the 70s, so the data is basically nonsense).

The last and probably most pertinent point on inflation is again the governments and central banks of the world convincing you that inflation is going away/coming down over the next decade. Maths was never my strong suit 🤓 but you can NOT increase the money supply to the extent that they did during COVID and expect inflation to come down.

Most of the people I respect and follow in the finance space continually point to the historical precedence of inflation, and how it usually always comes in three large waves. IMO, we have only seen the first of these waves (this ties into my next post on How I Invest - you need to own real assets to protect yourself from inflation, i.e commodities).

You need to ability in the future to increase your cashflow, substantially - and you want to be at least double the RR of inflation. Relying on passive dividends does not give you much/any control over this.

FIRE Rant Summary

So, essentially what I am arguing is that if the primary point of FIRE is living off passive dividends, why not search out a much better ROI than 4% once you have spent 20+ years of your life amassing over 1 million dollars!

I feel these FIRE people are so blinkered into this 4% passive narrative. To me it actually seems super risky not to put a huge lump sum of capital to work (or at least a portion of it!) on a higher ROI. 🤷♂️

4 - Peter Thornhill 📖

Motivated Money by Peter Thornhill was a book I discovered at around age 27. I strongly recommend this book to all Aussies out there who want an alternative view to the property narrative. This is basically an alternate view on FIRE, so my same above issues apply, but nonetheless it is a good book.

I don’t agree with everything Peter advocates, especially given how I think about investing now, but he is essentially very pro stockmarket investing (mostly in LICs for income) and very anti-property investing. It is refreshing for an Australian to read this alternative, well-articulated point of view.

He is basically a rich old dude with an 11 million dollar portfolio (amassed from $0), with no tertiary education, after working his way up in the financial sector from a clerk to a consultant over 40 years. 11 million dollars of LICs gets you about 500k of dividends annually (fully franked, won’t explain that here, look it up). Yes, I would concede that the 4% rule IS applicable if you have >$5 million 😅

A brief thought experiment on 11 million dollars…. (An example of The Coal Trade)

If I had 11 million dollars, I could put 3.5 million into a basket of coal-mining companies (another idea from TraderFerg) to pump out the same dividends of about 500k per year as 11 million in LICs (with lots of additional potential capital gain upside). This would leave me at least another 7 million dollars to invest in anything/everything else! As usual, I digress..

Stumbling across Peter’s book after hearing him on a podcast completely solidified my thoughts on Australian property at the time. Motivated Money was important in the evolution of my investing philosophy as it gave me a slightly nuanced alternative to the FIRE movement.

5 - Asymmetrical Investing 📈 Doing a 180 on My Investing Philosophy

Initially I’d planned to put this in this article (this was to be the meat and potatoes), but given I’ve managed to rant over 4,000 words already I’ll make it a separate post.

Doing a complete 180 on my entire way of thinking about investing

As outlined here, I Met

through my mate when I moved into a villa with them in Bali in 2019, during my time off from working at an underground nickel mine in Western Australia.I started to listen to

s investing ideas in 2019, particularly through his old free newsletter, and these articles and links is what catalysed my thinking slowly into the idea of investing in cyclical, asymmetric sectors over the course of 2019 and 2020. This let me down the rabbit hole of discovering other contrarian pundits in the financial space, who I’ll mention in the next article.Asymmetrical Investing (briefly)

The simple idea that certain sectors go through continuous multi-decade cycles, which continue to play out with time, but are usually forgotten about by the mainstream financial pundits. This type of investing that Brad, Chris and

look out for involves identifying hated, ‘bottom crawlers’ (charts) in a certain sector (e.g. uranium, coal, dry bulk shipping); looking at the fundamentals within the sector to see if it is about to begin its long cyclical trend from ‘forgotten’ to ‘in vogue’, or from ‘really fking awful’ to ‘just awful’ (where the most money is made).

Summarised Above

Late 2019 - Started to get convinced to take more risk; wanted to enter the uranium trade.

2019/2020 - Stubbornly and stupidly had the idea that I wanted to hit 110 - 120k in passive ETF’s in the portfolio, before diversifying into ‘riskier’ single company stocks.

2020 - Started my first (small) positions in uranium during the COVID crash.

Slowly convinced myself of

s style of asymmetrical investing over 2020 as I learnt more about it, and began pivoting into uranium and offshore oil drillers.Saw a few of my mates make some huge returns off the initial moves in uranium in 2020. Finally questioned my philosophy on the whole FIRE movement.

Early 2021 - dumped everything into uranium and offshore oil, but still missed the big asymmetrical moves off the bottom (a hard/good life lesson here).

Kept adding as much salary as I could afford.

2022 - finally saw the portfolio grind higher. Started to take some small positions in coal mining companies (more on the coal trade in the future), but still putting most of my salary into uranium and offshore oil.

More on asymmetric investing in the next post.

6 - Travelling & Playing the Waiting Game ⌚

Already talked about this here. In June 2023 I had enough capital with no debt to comfortably quit my job and go travelling for the long term - as a direct result of taking on some more risk while young, finding some contrarian financial mentors to follow and investing in asymmetrical energy stocks.

This is not for most people, but it is perfect for me as it gives me the most flexibility and freedom at this stage of my life.

The rest of 2024 will be spend ‘geo-arbitraging’ life, travels and expenses in Latin America. Keeping in mind that I’m not living like a monk, and I have not stayed in a single shared style accommodation since I left. I had about 30k worth of shares in shipping and misc companies that I slowly scaled out of for a small profit over 2023/24, helping to fund my travels.

I’ll continue to write monthly life and networth updates for anyone interested.

7 - Wrap Up & Future Financial Plans

As

and many others have stated, there is a high likelihood that uranium will do something silly in the next 6 to 18 months (I really hope this happens in 2024… 😆).Plans on exiting uranium.

This will be another future post too 📫

In December I’ll return home to Tasmania for at least a month to see family. My plan is to try time it by starting to take some slices off the uranium side of the portfolio during 2024/25 summer (famous last words).

Indeed, with the Australian Labor government’s new reduced tax brackets for financial year 2024/25, I’ll likely plan on at least maxing out close to the new 190k threshold before July 2025. If uranium has a super spike, then I’ll probably just dump most of the shares in FY24/25 and cop the tax (will still be better off), but if it continues to grind through volatility, I’ll consider to scale out slower throughout financial years 2024/25 & 2025/26.

The Offshore Drillers side of the portfolio is only just starting to move now, and I expect this to have a minimum of three more years to run, likely up to 5 more years. I’ll probably use at least 10% of the uranium gains to add to positions in offshore, if buying opportunities arise.

The Coal side of the portfolio is still very small, only about USD $20k. I would like to get this up to $100k minimum by 2025 at least (using again some of the uranium gains). This is a long-term, 10 year ish play that I hope to add to over the next 5 years.

Plans for cashflow in the future 💵

I have big plans in the future to hopefully drop a minimum of $300k (of uranium gains) into buying a portfolio of websites for cashflow, over the next few years. This is a completely separate topic that I will write about in the future. During 2023 I did a website SEO course run by a wealthy Australian angel investor couple. This course/community blew my mind in terms of ROI from profitable websites.

Essentially $100k invested into a profitable website with a solid track record will yield and ROI of about 30% annually, or about $2.5/3k per month, with lots of upside once you renovate the website. By spending $300k on online businesses I can essentially buy my way to freedom, as this would easily yield a minimum return of $10k per month (with upside).

Cashflow (from my laptop) will become the most important financial aspect of my life once I am out of uranium. Combine this with the longer term goals of getting out of the Australian tax system legally, and you can start to see my vision for the future.

El Fin 🙋♂️

A long rambling post - thanks to anyone that read this far. Appreciate if ya hit the like button! 💗

Cheers - Van Diemen

Great article, enjoyed reading it!

Agreed, great read and looking forward to more to come in the future. Thank you